One question comes up in nearly every conversation I have with transit agencies considering open payment: “If riders can simply tap a credit card to board, how does my agency know we will actually get paid?”

One question comes up in nearly every conversation I have with transit agencies considering open payment: “If riders can simply tap a credit card to board, how does my agency know we will actually get paid?”

It’s a fair question and one that’s often misunderstood. Open payment isn’t designed to eliminate payment risk. It’s designed to manage a small amount of industry-standard payment risk in exchange for dramatically improving the rider experience.

Once you understand how the payment process works behind the scenes, that tradeoff becomes much easier to evaluate.

Comparing the benefits of open payment to the risks

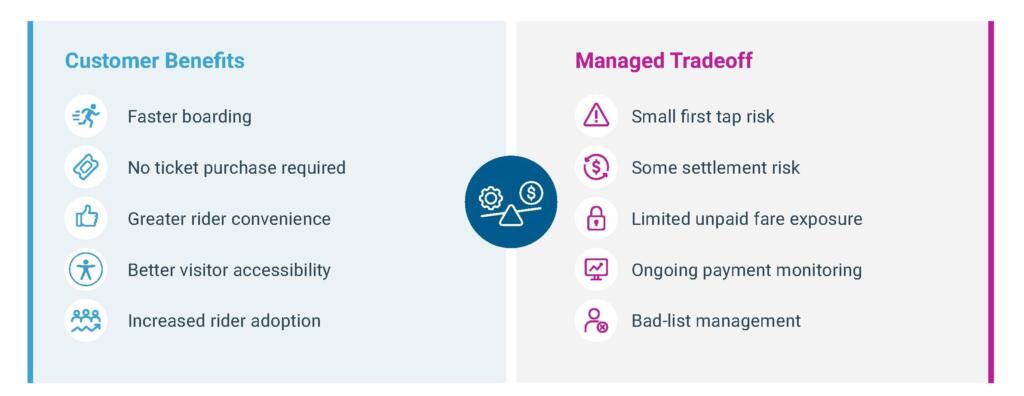

If payment isn’t guaranteed, why are so many agencies adopting open payment? Because the operational and customer benefits consistently outweigh the relatively small amount of managed payment risk.

Open payment delivers benefits such as:

- Faster boarding and reduced dwell times

- Reduced driver interaction at boarding

- Less reliance on cash fares

- Greater convenience for riders

- Easy access for visitors and infrequent riders

- A frictionless customer experience that riders increasingly expect

Speed is prioritized over real-time authorization

Transit is unlike almost any other retail payment environment. When someone buys groceries or shops online, the merchant can wait a few seconds for the bank to approve the transaction before completing the sale. Transit doesn’t have that luxury.

Vehicles need to stay on schedule, riders need to board in seconds, and network connectivity isn’t always guaranteed while the bus is on its route. Waiting for a full payment authorization at every boarding would create delays that ripple throughout the system.

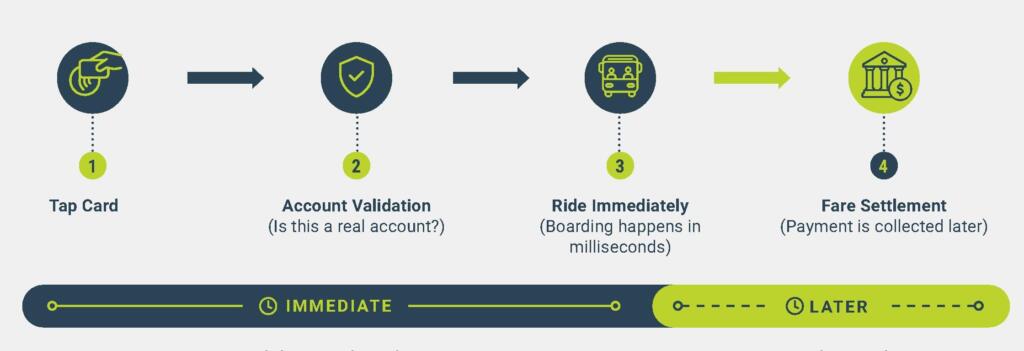

That’s why open payment follows a different model. Instead of waiting for final payment approval before boarding, the process takes less than 300 milliseconds and looks like this: Tap → Validate → Ride → Settle

When a rider taps their contactless bank card or mobile wallet, the payment system first validates that the account appears legitimate. The rider is allowed to board immediately, while the final payment is processed later through the banking system.

Validation reduces risk but doesn’t guarantee payment

The distinction between validation and settlement is important to understand. A successful tap doesn’t mean payment has already been secured. Validation simply answers questions like:

- Is this a legitimate account?

- Is the card expired?

- Has the card been reported stolen?

- Is the account currently in good standing?

It does not confirm the current balance of the account or whether sufficient funds will be available when the final fare is collected later. The payment network simply confirms that the account is legitimate.

2 types of payment risk

Because transportation is provided before payment is finalized, transit agencies manage two primary types of payment risk.

First tap risk

First tap risk occurs when the payment network determines that the account is lost, stolen, or otherwise invalid after the ride occurs, such as due to connectivity delays. Fortunately, this type of risk is reduced greatly by the typical validation process and represents a small portion of overall open payment exposure.

Settlement risk

Settlement risk is more common. In this situation, the card passes the initial validation, allowing the rider to travel throughout the day. Later, when the transit agency submits the accumulated fare for payment, the bank declines the transaction because sufficient funds are not available.

Again, the transit service has already been delivered, creating a small amount of revenue that needs to enter the debt recovery process.

How open payment risk is managed

The open payment process includes multiple layers of ongoing risk management. For example, if a card fails validation or settlement, it is added to a bad list that is distributed to validators and fareboxes. Future taps from that account are rejected until the outstanding balance is resolved or the account status is cleared.

These controls help limit continued exposure while ensuring legitimate riders continue to enjoy a fast, seamless boarding experience.

Debt recovery strategies

There are multiple ways for agencies to successfully recoup whatever is left on the balance, such as:

- Automated, tap-initiated debt recovery. If a card is recognized as holding debt, it can trigger upload from the farebox to the cloud right away and require a first tap for what the rider owes and a second tap for the current ride.

- Bulk manual retry for debt recovery. The agency can upload bulk retries on a regular basis, aiming for common payday schedules in the area to improve recovery.

- Setting thresholds for tap attempts. Genfare Link allows agencies to specify how many times a new or denied card can be tapped for immediate authorization, which can prevent transaction fees from being charged to the agency.

- Give riders a payment portal option. The agency’s fare collection solution can be set up so that riders can go to the e-Fare portal to settle their debt, taking them off the bad list.

Microtransactions = minimal risk

Another question I’m asked frequently is why transit agencies can’t use open payment to sell printed multi-ride passes like day passes or weekly passes. The answer comes back to risk management and whether speed or security are prioritized.

Open payment is designed for microtransactions without real-time authorization, prioritizing speed. Open loop payments are for retail transactions of any size and are authorized in real time, prioritizing security. These types of transactions have different risk profiles.

With tap-to-pay single rides, if the settlement fails, the potential loss is small enough to justify the benefits.

Issuing a printed day pass, weekly pass, or other standalone fare product carries a greater risk. If the payment ultimately fails, the rider still possesses a valid pass that can continue to be used, making the financial loss larger.

That’s why transit agencies can’t issue multi-ride fare products purchased with bank cards or mobile wallets at the farebox. These transactions need to happen at retail outlets such as point-of-sale terminals or ticket vending machines or use e-commerce platforms such as mobile apps or online rider portals that use real-time authorization. This makes sure payment is fully authorized before the product is delivered.

Modern payments require modern risk management

Every payment system carries some level of financial risk. Open payment is no different. The difference is that today’s transit agencies have proven tools, established industry standards, and effective risk management practices that allow them to confidently deliver the convenience riders expect while protecting revenue.

And it’s getting better all the time – Genfare is always developing new features and on the lookout for additional ways to minimize unrecoverable revenue, improving the open payment experience for both riders and transit agencies.

Understanding how validation, settlement, and ongoing payment monitoring work together helps agencies make informed decisions about deploying open payment — and explains why agencies around the world continue to embrace it as a cornerstone of modern fare collection.

Vicky Tuan is the payment processing manager at Genfare.